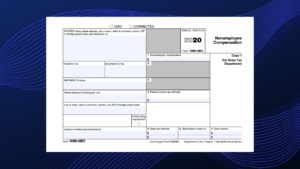

Businesses Beware: Despite COVID-19, the Internal Revenue Service is moving forward with changing the reporting requirements of Form 1099-MISC box 7, “Non-Employee Compensation” requiring reporting instead on Form 1099-NEC, effective for 2020.

Businesses Beware: Despite COVID-19, the Internal Revenue Service is moving forward with changing the reporting requirements of Form 1099-MISC box 7, “Non-Employee Compensation” requiring reporting instead on Form 1099-NEC, effective for 2020.

Although Form 1099-NEC is straightforward, Box 1 is for reporting Non-Employee Compensation, many businesses will now be required to also file Form 1099-MISC to report amounts paid for other types of miscellaneous payments such as rents, royalties and legal fees.

While there are many types of information returns that businesses are required to file, the most common for our business clients in the past was Form 1099-MISC. In fact, according to a 2019 NPR/Marist poll, 20% of American workers were contract workers, a trend that continues to be on the rise.

We anticipate this change in reporting will add to the complexity of reporting requirements for businesses since they may now need to navigate through two different tax forms, with two sets of instructions and two different due dates.

Filing Requirements for Form 1099-NEC

Generally, you should file a 1099-NEC form for all vendors that are not incorporated and to whom you’ve paid $600 or more during the calendar year. Your list likely includes individuals, partnerships, LLCs, LLPs and some corporate entities, including contractors and non-employees.

While generally the 1099-NEC is due to be filed by January 31, to both the recipient and the IRS, for 2020 the due date is February 1, 2021, since January 31 falls on a Sunday.

Specific instructions for Form 1099-NEC can be found at www.IRS.gov/Form1099NEC

Who NOT to issue Form1099-NEC

Do NOT include amounts paid to vendors via credit card or debit card in the totals reported on 1099s. The credit and debit card companies will already be reporting this income to vendors.

Remember: This requirement applies only to businesses. If you make these or similar payments as an individual, not a business, you are not required to issue a 1099.

Filing Requirements for Form 1099-MISC

File Form 1099-MISC (Miscellaneous Income) for each person or entity to whom your business has made the following payments during the course of the year:

- At least $10 in Royalties (see the instructions for box 2)

At least $600 in:

- Rental Payments (box 1)

- Prizes and awards (box 3)

- Other income payments (box 3)

- Fishing boat proceeds (box 5)

- Medical and health care payments (box 6)

- Payments to an attorney (box 10), regardless of whether the attorney/firm is incorporated or not incorporated

- Direct sales of at least $5,000 of consumer products to a buyer for resale anywhere other than a permanent retail establishment

Additionally, you must also file Form 1099-MISC for each person from whom you have withheld any federal income tax (report in box 4) under the backup withholding rules regardless of the amount of the payment.

Specific instructions for Form 1099-MISC can be found at www.IRS.gov/Form1099MISC

At SJG we can help you navigate thru the ever-changing tax landscape. See our last blog on Form W-9 best practices: https://www.sjgorowitz.com/irs-form-w-9-best-practices/