We’re seeing a significant demographic shift shaking up the small and middle-sized business (SMB) market. As Baby Boomers are aging and retiring, many are looking to sell their businesses, which represents a significant opportunity for would-be entrepreneurs to explore a chance at business ownership.

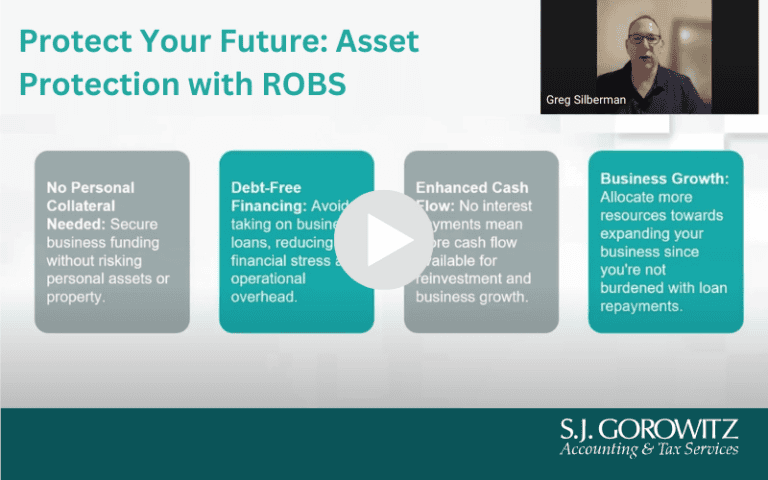

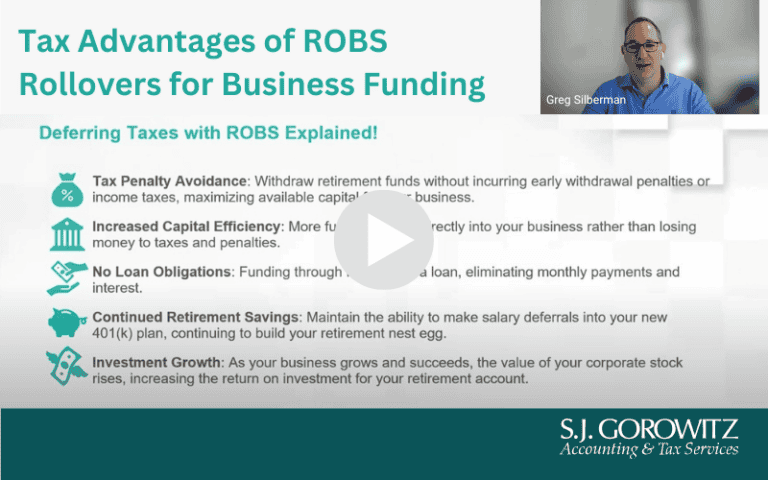

Finding the capital to buy or start a business is a critical first step. In our series on Rollovers as Business Start-ups (ROBS) for starting or buying a business, we’ve explored how ROBS provide access to cash flow, tax advantages, debt-free financing and asset protection benefits.

As a reminder, a ROBS strategy is a capital creation mechanism that accesses your 401(k) early, without any penalties. You can use the money from your 401(k) to invest in a C corporation that you will own and manage and may use to buy subsequent companies.

ROBS and Wealth Protection

Many people ask, “When I use a ROBS strategy, does my 401(k) have to own 100% of the C corporation?” The answer is ‘no.’ The C corporation is an operating company that can be owned by other entities, including taxable entities or other retirement plans that you own.

One use of the ROBS rollover is known as the 80/20 split. In this scenario, your 401(k) rollover can own 80% of the C corporation, while the other 20% is owned by another entity.

By using ROBS and having your Roth IRA own part of the new C corporation, you’ve likely shielded yourself from $180,000 in capital gains.

Benefits of the ROBS 80/20 Approach

Creating a business ownership structure that includes funds from qualified retirement plans, like 401(k)s, Traditional IRAs, Roth IRAs and SEP IRAs, offers some key benefits:

- No mandatory distributions. When you use a ROBS strategy to finance or start a business, you are not required to begin taking Required Minimum Distributions (RMDs) at age 72. Not having to take RMDs allows your wealth to grow tax-free for a longer period.

- Higher net worth accumulation and greater financial legacy. By shielding your financial assets from tax liabilities, you can accumulate more money to transfer to heirs and beneficiaries in the future.

- Tax-free wealth transfer. Up to 100% of the gain on the sale of a business can be passed on to heirs without incurring estate or inheritance taxes. When the business owner passes away, their Roth IRA gets a step-up in basis when distributed to heirs, thereby avoiding inheritance tax.

In short, shielding assets from tax liabilities using a ROBS strategy can provide a measure of lifelong wealth protection for your spouse and future generations.

If you’re interested in taking the next step with ROBS, S.J. Gorowitz Tax and Accounting Services would be pleased to offer you a consultation on your business plans and objectives. Please contact us at 770.740.0797 or email info2@SJGorowitz.com.